|

Deal valuation is something that many executives struggle with, and I probably get more questions on this topic than any other. This is understandable. Acquisitions are big decisions that can make or break an executive’s career. They are often competitive, with multiple bidders. Investment bankers, with their deal experience and complex models, can be somewhat intimidating for many, making it a scary proposition to start questioning their numbers. It is nevertheless critical to make sure the valuation is calculated properly, thoroughly vetted by management, and well-articulated to the board. The best place to start is to return to the foundational basics we’ve discussed in earlier posts:

While it may seem tedious to keep returning to these B-school basics, it is extremely useful to do so as it helps inoculate against the “deal fever” that so often leads to overpricing and poor investment decisions. Buying a company should be like buying anything else for your business, a new photocopier or another delivery truck. “Will the purchase accomplish our objectives better than another approach or investment” is what you are seeking to answer, and the bias should be towards skepticism and objective logic. And you can tell those scary bankers that I said that! Re-grounded in the strategic basics, with our “deal fever” booster shot, we can get down to the business of some calculations. Two common methods used to calculate acquisition valuations are comparable multiples and discounted unlevered cash flows. We will discuss multiples here, and cash flow valuation in a future post. Comparable multiples Regardless of what other valuation methods you employ, you will likely need some comparable multiples for your board and/or investors to consider. Multiples are calculated thus:

This gives us an average valuation of 10.6 EBITDA, and a median valuation of 10.0 EBITDA, which when applied to our target’s financial results yields the comparable value. Real-World Example: Nothing Can Compare Several years ago a CFO asked me if I could take a look at the valuation model for a proposed deal. I agreed, but immediately ran into some noticeable resistance when I contacted the bankers and requested a copy of the model. When I finally got my hands on a copy, the reason for their hesitation became clear. Their figures showed sales revenue for the proposed target increasing at 6% per annum in perpetuity! Nice, but hardly likely. I immediately set a meeting with the bankers, and asked them to provide the business operations and market research rationale that indicated the business would grow forever. Not surprisingly, they were unable to provide such analysis. Eventually they admitted that the 6% perpetual growth was simply “the formula we had to put in to get to the multiple a competitor recently sold for”. To make matters even stickier, the same bank was representing a party that would benefit from the higher sales price, so definitely a cagey situation. Luckily, in the example above we were able to calculate a more realistic projection of the company’s prospects, and narrowly avoided overpaying for a terrible investment. Remember to always check the deal models, and to validate all assumptions! The problem with multiples is the underlying assumption that all parties were rational actors, and that the amount paid for the company was highly correlated with EBITDA. This is not always the case- in fact many tech and pharma acquisitions are done before there is any profit, and sometimes even before there is revenue! This is also exactly how asset bubbles develop, and I would strongly caution against evaluating deal value based solely on what others have paid. Also, the 10.6x above is not what the deal is worth to us, it is just what we might expect to have to pay. What it is worth is another matter altogether, but we know that because we’ve reviewed our strategy fundamentals. Right? That said, multiple comparisons do have their uses. First, due to different strategic priorities and deal rationales, it would be reasonable to expect an acquisition to be worth more to certain parties than to others. Considering the median/average values of multiple transactions can help predict the range of values that your competitors might be willing to pay, and (perhaps more importantly) what your investors might be willing to fund. So multiples are a reasonable starting point, but don’t get stuck there.

0 Comments

Elaborating on diligence execution in detail would be a book in itself- after all, as previously stated, my standard questionnaire is 30 pages long! We will instead provide a high-level overview, looking across the various categories, and taking account of key elements that warrant focus. Diligence Topic 1: General Items General items usually include at least the following:

Watch carefully for significant omissions and surprises in this early area of diligence. In my experience these indicate a large “red flag” with regards to the rest of of the process, provided there were earlier forums in which it would have been reasonable for the target’s leadership to be more forthcoming. Apart from hostile transactions and or distressed targets, diligence should not be an exercise in obfuscation on the sell side and in teeth-pulling on the buy side! How a buyer should respond depends on the deal rationale. The more likely it is that you will need to rely on the target’s existing leadership for full synergy realization, the more concerning any early-stage deceptions or omissions. At a minimum, such behavior should be considered when calculating the deal pricing and synergies, as deception is seldom a one-time behavior. Diligence Topic 2: Finance and Tax You should get Tax involved in the diligence process early and ensure that they are provided with copies of the target’s legal entity structure, including details on any international operations. This will allow them to design an approach that minimizes compliance exposures and tax costs. Carryforward items are also critical to evaluate early on, as these can have a very significant effect on deal value if the client has had large operating losses in prior years. I once worked on a deal with a purchase price of several billion dollars that was nearly entirely funded via tax savings from proper deal structuring and capital planning. Conversely, I am aware of another deal where several hundred million in avoidable tax costs were incurred because Tax was not allowed to participate in diligence. With regards to the rest of financial diligence, auditors often lead the charge; however, it is important to have skilled personnel from your internal Finance organization involved as well. The auditor’s role will be to carefully analyze the provided information for completeness, accuracy, and any potential red flags. Internal Finance staff should review the auditor’s inputs carefully and raise any concerns with Leadership including the Steering Committee, the Integration Lead, and Corporate Development. Here again, there should be minimal surprises. In addition to the above, your internal Finance resources should also be evaluating the consistency or inconsistency of policies, processes, and tools as compared to your internal structure. In this way, Finance can begin to evaluate the time and effort required to achieve your desired TOM and can inform the Data Steward of any potential data migration/integration requirements that need to occur in time for the first consolidated close. I also recommend assigning one internal resource to carefully review the financial data and reconcile it to all deal models and projections. You would be surprised how much I see omitted and misrepresented in deal models, when the information from diligence clearly refutes these assumptions! Diligence Topic 3: Legal Compliance If you are using an experienced outside counsel to assist in the diligence process, this portion usually goes smoothly. If you are using inside counsel, be prepared to augment their staffing and their experience with outside experts, particularly when considering cross-border transactions. Make sure all attorneys involved are aware of any red flags uncovered in your research. Diligence Topic 4: Legal Contracts It is my experience that contracts frequently get under-researched during diligence. Migration/novation of contracts: customer, subcontractor, contract manufacturer, and/or outsourcer, can easily be the “long pole” in many integrations, and usually comes at the expense of significant investment in both time and legal fees. Pay attention to any restrictions on assignment, novation, or termination as these may bind you to a model that differs from that of your desired TOM. Also, pay close attention to any contractual arrangements that might inhibit your ability to alter pricing or costs of inputs! Inquire as to whether any verbal representations have been made to customers and/or vendors regarding terms or pricing. If the client in our “Double Trouble” example (see March 2018 blog) had included this in their diligence research, they would have known that there was no legal way to raise pricing after the acquisition. Also, if your value proposition includes substantial benefits from cross-selling, pay attention to contract overlap with your existing customer base. It could be that you have captured most of the TAM (total addressable market) already and thus the acquisition is of little additional value. Diligence Topic 5: Facilities Facilities diligence should bring to light risks in areas such as environmental and/or safety hazards; furthermore, it should also assess whether the facilities present any obstacles for your chosen TOM. Are you planning for shared occupancy for a period of time? Then note whether the space can be easily demised, with proper access controls and security. During facilities walk-throughs, also take note of any fixtures that are of interest. I once spent weeks arguing whether a satellite dish affixed to the roof of an acquired building (and necessary to continued operation of the business) was included in the scope of the facilities purchase! Other such items might include warehouse racking, videoconferencing equipment, conveyor systems, etc. Ensure any such assets get called out specifically on the asset inventory in the purchase agreement. Diligence Topic 6: Insurance & Risk Investigate whether adequate coverage is in place. Companies that skimp on insurance coverage may be risk-prone in other areas as well, so it is worth noting. If the company self-insures, they should have an adequate reserve for any potential losses. Also, make sure in this instance that your broker or insurance company is willing to write the policies you need for an acceptable cost. Before completing diligence in this area, review your PESTLE assessment one more time and determine whether additional coverage or mitigation investments are appropriate. Diligence Topic 7: Employees, Benefits, & Pensions Employee and benefits due diligence is often a massive effort, so plan to invest in this area accordingly. It is also worth doing well, and not just from the standpoint of risk mitigation. Employee diligence provides the first real opportunity to dig into the details of what the acquisition will mean to the target’s staff, and to glimpse how day-to-day culture and practices at the two companies differ. Perhaps more than any other area, employee diligence provides also informs major components of the integration plan, including what change management and communications activities may be required. Given the scope of this effort, and its potential payoffs, I recommend staffing diligence with top personnel from HR, backfilling as needed to cover any gaps. Also, be flexible about allowing the diligence staff to bring in consultants to assist, and to hire employment attorneys to advise them. Diligence Topic 8: Competition, Control, & Corruption Turnover is one diligence area that falls under the competition portion of this heading. You will want to carefully review company revenues, gain an understanding of what their total market share is relative to their competitors, evaluate how much of that share is due to joint ventures/alliances/partnerships, and how great the dependencies are on particular channels and/or customers. If the company operates in more than one geography, it is also key to note whether one country is disproportionately responsible for overall turnover. For the control and corruption portions of this heading I would suggest that you review at least the following:

Careful diligence in this area is not only a requirement, but also a useful preparation for anti-trust approval discussions with regulators. Ensure that this area is staffed with attorneys that have adequate diligence experience in the markets in question and instruct them to openly share information with your anti-trust counsel, facilitating these discussions periodically.

Diligence Topic 9: Information Technology Note that while extensive detail regarding the IT and telecommunications infrastructure may not be required if you plan to minimally integrate, it is still a good idea to get a view of the systems landscape. Information and data security compliance is growing ever more complex, and the expectations and potential liabilities for breaches are growing as well. As with the more general areas of diligence, a careful look under the hood is appropriate, since carelessness can indicate a bigger problem with a lack of business discipline. If you do plan to fully integrate, there is a good chance that systems and data integration will be both the longest-running and most expensive portion of your integration plan. As such, it is a good practice to have your Data Steward in place and participating in due diligence, along with any other internal or external augmentation required. Recap Due diligence is an intense, complex, and time-consuming effort, regardless of the acquisition. If you are considering a full-integration TOM, diligence should also become the first phase of your planning activity, informing each group as to the likely scope, timing, and extent of the effort required. You will want to ensure that you have adequate participation to not only cover the scope of the diligence activities, but also to have time to share the information learned along the way, and to discuss how this might impact the realization activities. For large deals, or deals with full integration TOMs, this may well mean augmenting existing staff with external contractors to ensure adequate coverage. Of course, the larger your diligence team, the more essential it is to have your program structure in place providing a forum for collaboration and governance. The Due Diligence Objective In our February 2018 blog post we noted that every successful acquisition starts with the identification of the deal rationale, or the “why” of the deal. This rationale should drive all subsequent activities including the approach to due diligence. First solidifying the business objective, and subsequently analyzing the target to assess whether it will help achieve that objective, can prevent missteps such as the “Double Trouble” example from our March 2018 post. Our goal, therefore, is to evaluate the target company to determine whether acquiring this company addresses our deal rationale objectives, while simultaneously getting comfortable that the risks are not sufficient to erode the overall value proposition. Conduct Due Diligence Research Most integration professionals will have a standard due diligence “checklist” of items that the buyer would like the seller to provide for evaluation. Mine is just under 30 pages in length, single-spaced! On a large deal I will usually get to submit less than half of the questions on my list, and for smaller deals I might be able to submit only 15-20%. So, one critical early step is to pare the list of inquires down to something that is manageable but still provides sufficient information to evaluate the target. Spending a few hours on research is one way to effectively whittle down the checklist. You would be surprised how much information is available via:

Buyers can be reluctant to invest the time in this research; however, I find it often yields a treasure trove of information that can be used to answer some diligence questions preemptively, and certainly helps to focus the diligence checklist! If you don’t have time to do the research yourself, bring in a temp or an intern. The work isn’t difficult and it is well worth doing before you commence with decisions about designing due diligence scope. I once found information on an industry blog about a well-known defect in a target’s primary product, which had not previously been apparent from any of the provided documents, and which had a material impact on some of the valuation assumptions we were using. Bottom line- take the time to dig- it’s worth it. Use PESTLE to Further Refine the Diligence Plan After compiling research, a useful starting point for scoping due diligence is to revisit some basic strategic frameworks. If you’ve been following the method we discuss in this blog you will already have used Porter’s 5 Forces and SWOT in your initial target identification. For diligence purposes the PESTLE (sometimes spelled PESTEL) framework is useful. PESTLE is an acronym:

Political risks usually take the form of potential changes in regulations or policies. Health care and social media are good examples of industries facing political risks. Economic risks are pertinent to businesses with commodities exposure, heavy reliance on discretionary consumer spending, foreign currencies, or other key economic factors. For example, these are significant considerations when I do deals in the international oil, gas, mining, or food/beverage industries. Social/cultural risks relate to the potential for loss of goodwill, litigation, or eventual political exposure due to negative public perception of the company or industry. I’ve seen this in media and entertainment with regards to violent content, and social media is definitely facing scrutiny here as well, as are processed food companies. Technological risks arise due to the disruption of existing businesses by emerging technologies. Who would have imagined 10 years ago that we might have self-driving vehicles? As robotics and automation improve, most industries will need to consider technological disruption to some degree. Legal risk refers to current or potential litigation risks. These aren’t always a bad idea. I’ve seen bargain purchases of companies that were facing litigation exposure, but risks should be thoroughly investigated in diligence so that valuation can be properly adjusted. Environmental risks are critical in resources businesses like oil, gas, timber, and mining; however, depending on the political environment any company can incur substantial changes to their cost structure due to environmental regulations. Determine Participants for Due Diligence There are conflicting schools of thought when it comes to participants for due diligence. Strategy and Legal experts seem to prefer as few participants as possible, while Finance and Operations want to see broader representation. Here again the deal rationale and its corresponding TOM can offer guidance. If the TOM calls for minimal integration, you should need fewer diligence participants. Where the TOM calls for medium to full integration, you should consider putting a larger team in place. Regardless, the best results are produced when the diligence team is broad enough to validate TOM assumptions, and to analyze the deal in terms of the deal rationale. This is the one reason I advocate for the use of code names, and for a thorough onboarding process for diligence resources. Keep in mind that work done to eliminate a deal from consideration is not “wasted effort”, it’s production! Rationalizing investment choices is a legitimate activity, regardless of the go or no-go decision resulting from the analysis. Should the decision be to move ahead with the deal, a properly organized and executed diligence process generates a significant portion of the integration plan and budget, thus saving time later in the process. Appropriate participants will vary by deal, but some general guidelines are as follows:

Note that the recommended participation, even for minimum integration, still extends across quite a few areas. We’ve spoken before about the importance of including Tax to ensure that the deal is structured in the most efficient way possible. Legal and HR are required to ensure compliance. Finance will be key to analyzing deal value, providing modeling inputs, and establishing synergy measures. The Integration Lead will be responsible for overseeing realization of the chosen TOM and the corresponding synergies.

Recap Take the time to research publicly available information on your target. Apply the results of your research using some standard strategic frameworks, incorporating all this information into the on-boarding materials for your diligence participants. Let the TOM inform the composition of your diligence team, but don’t hesitate to include more resources- the broader participation should pay off in terms of better results. Getting Started with Due Diligence The first step in preparing for diligence is often deciding what the deal or project will be called. I am an advocate for creating code names for the deal and each of the participants. The purpose of this is twofold. First, it provides an additional layer of security against information leakage during the critical and confidential period prior to announce (you would be surprised how much I overhear about deals in airports, hotels, and coffee shops!). Second, assigning names outside of the terms used in daily discussions helps to produce a “fresh” approach to diligence, shake resources out of their day-to-day thinking patterns, and define the acquisition as a project. Have some fun with it. Why not a Project Cheeseburger with parties such as Pickles and Mayo? Regardless of whether you choose to use code names or maintain the actual names of the parties you will need a robust on-boarding process for diligence that features the following:

Program Structure

It is advisable to set up your acquisition program structure in advance of diligence. Even if the acquisition doesn’t go through, the effort undertaken to setup a subsequently-abandoned program pales in comparison to the wasted effort and potential risks of trying to run diligence with no structure in place! There are 2 basic ways to organize an acquisition program. The first is an objective structure, where various cross-functional “tiger teams” are formed to accomplish program objectives. If your resources are accustomed to being allocated to various projects with different leads and objectives on an ongoing basis (i.e. similar to Google) you might prefer an objective program structure. The second is a functional structure, where the teams mirror the traditional internal functions of the company (finance, technology, marketing, etc.). A functional structure has the advantage of being much easier to setup and govern than an objective structure, because accountability rests with functional leadership for both ongoing operations and integration activity. For this reason, functional structures are far more common than objective structures. Regardless of which is selected be sure to consider whether performance measures, compensation, and/or incentive structures need to be adjusted to reflect changes in responsibilities. Steering Committees A steering committee or committees is the preferred method of program governance. The key idea for “steerco” setup is that the steering committee members must either be C-suite executives or have access to the C-suite. Smaller companies often have the CEO, CFO, etc. serve on the program steerco. Larger companies often opt to have C-suite direct reports on an operating steerco, with the C-suite resources instead serving on an executive committee that meets less frequently to take major updates, greenlight decisions, and manage high-impact escalations. For diligence purposes it may be appropriate to have a higher level of executive sponsorship on the steerco, and then have a direct report delegate take over later in the process. If you are using a functional structure, the steerco will be easier to design. Simply pull an executive from each function to represent his or her group. If you are using an objective structure, forming an effective steerco is a bit trickier. You need to select members that can lead each of the objective workstreams. This requires selecting executives that have significant cross-functional span of control, but also a high level of accountability for the achievement of the outcome in question. In other words, they must both care whether the objective is achieved and have the (practical and political) means to do something about it. Remember to set your steerco up in time to get their input on the diligence process and kickoff materials. And don’t forget to require the steerco members to complete the NDA process. Really! Most of the blabbing I overhear in airports comes from very high up the ladder, and everyone benefits from a reminder to keep things buttoned up. Once the NDAs are signed, walk the steerco through the problem statement, deal rationale, and TOM assumptions to ground them in the basics of the deal and get their feedback. Tools O’ The Trade Your attorneys will likely provide the due diligence data room. This will quickly become a morass of documents, all organized in a structure that only lawyers and aliens from the planet Nebu can understand (in reality the data room structure is often tied in some way to the numbering system of the due diligence requests and/or questionnaires). As such, taking time to agree with your attorneys on a structure and numbering system for these documents can prevent confusion and save a great deal of time that would otherwise be wasted searching. You will want your own repository for non-confidential documents such as kickoff decks, status reports, training materials, etc. Take the time now to set up the tool of your choice, i.e. SharePoint, Box, Dropbox, or other. This will make coordination and communication during diligence easier and carries over nicely to integration should the program move forward. Loading any existing deliverables you have accumulated to date, i.e. documentation of deal rationale and TOM assumptions, is a good idea. Recap Take the time to do some basic program setup, including establishing tools and governance, prior to commencing diligence. This will improve coordination and yield better diligence results. Make sure to design a robust onboarding and NDA process, and to have platforms in place whereby resources can obtain and share materials. Data and Automation

This topic used to be of concern only to the largest acquirers; however, technology adoption has advanced such that even smaller companies often operate on complex IT systems and leverage automated workflows for many business processes. As such, an understanding of the systems and data architecture of the parties is now both a key aspect of a thorough due diligence process, and a key structural consideration when selecting a TOM for all types of M&A. It is important to note that many large enterprise resource planning (ERP) systems, such as SAP or Oracle, are highly configurable and thus can be extensively customized by the installers. It is almost certainly a mistake to assume that because “both of us are on SAP” that your data structures are in any way compatible! Let’s look at an example: Target Company's General Ledger Account Numbering Logic is described as AB.CDE.EFGHI And: AB=country CDE= legal entity FGHI= general ledger account number Acquirer's General Ledger Account Numbering Logic is described as AB.C.DE.FG.H.IJKL And: AB= legal entity C= country DE= division or business unit FG= budgeting cost or profit center H= tax treatment for this account, often used for feeds to "bolt-on" tax calculation engines IJKL= general ledger account number Right away we can see that in order to do joint reporting, we are going to need to do some breaking apart and re-mapping of the target’s data, or else forego same and institute a manual process. (Side note- if we use outsourcing, any such manual process would likely require a new contractual agreement, since the current process for reporting leverages the existing acquirer data structure). Given the integrated nature of these tools it is common for multiple processes to share a single data field-even across multiple functions or even business units. Recall that the acquirer had a tax treatment field designed to export data to a tax engine. Such a field would often be used in the USA to send data to separate tools for sales tax and income tax, and outside of the USA might be used for both value-added tax (VAT) and for local financial statement reporting under that geography's GAAP rules. The field may also be used to exempt certain accounts from consideration in the budgeting process, i.e. to indicate accounts used only for intercompany transactions. Bottom line, be sure you have a complete understanding of the data map and the design of all interfaces and workflows before planning to change an existing data structure. Here I’ve provided the more difficult example, where the target’s existing data needs to be broken into smaller segments. This is more common since the acquirer is usually larger and more technologically sophisticated than the target; however, the opposite situation could also apply. In that case the exercise may be simpler, i.e. you can combine data more easily than you can split it out. In either case, you must take into consideration the time and resources required to consolidate on a combined toolset, and that will have an impact on your selected TOM. Note also that we’ve only looked at GL account structure in our example thus far. Imagine the scope that can occur across all of the parties combined data elements and data sets! This is the reason that data migration is often the “long pole” on the integration critical path, and why an understanding of data and systems architecture is a key consideration in TOM selection. By now you should have a good idea of how to design or adapt a Target Operating Model given the structure of your deal or deals, and your company’s propensity to acquire. The next step is to evaluate whether your chosen TOM is impacted by aspects of your company’s structure.

Shared Services Impacts For our purposes let’s define shared services as centralized administrative groups, usually located in low-cost jurisdictions, that perform back-office activities for much or all of the enterprise using an employee model. Whew- that was a mouthful, but the key phrase for TOMs is “using an employee model”. This generally means that acquirers have sufficient span of control over the shared service organization to adapt it to the needs of the integration. And indeed, most adapt fairly well so long as sufficient time and budget to achieve are provided. To assess the budget and timeline requirements certain key aspects should be considered:

Outsourcing Impacts Outsourcing is similar to shared services, except the activities are performed by third parties under contract rather than employees, and thus the span of control is limited. If either or both the buyer and seller use outsourcing, expect substantial time and additional costs to achieve the desired TOM due to the need to create new service contracts for the extraordinary activities resulting from the transaction. Try to get access to any outsourcing contracts early in M&A diligence- even if a clean room is required- so as to get a head start on the process of identifying the scope of required that will be required for TOM achievement. Also, be sure to consider capabilities of outsourced staff, and be aware that most outsources are reluctant to be flexible with regards to interim or exception processes. This means that more time will be required up front to design and standardize a process, enter into a contract to have the outsourcer perform the process, and train the outsourced staff. You will want to develop an integration plan that minimizes the number of transitions, which can be particularly challenging if your value drivers call for an interim TOM. Regardless, any TOM you plan to achieve will have to be well-defined and validated in advance, and you need to be prepared to operate in that model until the next well-defined transition can be executed- usually at least a few months. Bottom line: if either party uses outsourcing, you can anticipate less iterative flexibility and higher costs for TOM achievement than you would experience in a shared services model. A new Nearco blog post is coming soon. Meanwhile, if you are looking for more M&A reading I highly recommend the excellent blog on Deallawyers.com. This recent post on poison pills is an example of how good they are at striking a balance between depth and readability:

https://www.deallawyers.com/blog/2018/07/poison-pills-uh-thats-not-how-they-work.html If acquisitions will be a recurring component of your growth strategy, you may benefit from creating some standardized TOMs to more quickly assess deal scope and costs. How many, and what kind, will depend on your industry, and the variety of deals you plan to do.

Components of a Standardized TOM Recall that a TOM describes the “5 W’s” or Who will do What from Where on Which tools, When. In preparing standardized TOMs, it is possible to address these questions, as well as to add some additional parameters that make integration planning, estimating, and execution more repeatable and efficient. The following components should be considered for incorporation into a standardized TOM:

Note that while it is possible to create a quite sophisticated model if all of the components above are included, it is most likely only cost-effective to do so if many acquisitions are planned. Furthermore, in-house knowledge of the appropriate estimating factors, task lists, etc. will be limited unless several acquisitions have already been executed, or unless you conduct a program to determine these inputs. The effort and complexity of the standardized TOM is why most companies continue to use business cases to evaluate synergy and cost realization efforts. That said, it is possible to document standard TOMs that include only non-quantitative data, and this may also be of some use. Minimum TOMs Your minimum TOM should be just that. It should describe the minimum level of integration required to meet your legal, regulatory, and non-negotiable corporate policy requirements, i.e. public companies will have consolidated financial filing requirements. Regardless of whether you want to delve into the creation of sophisticated models, creating a minimum TOM is usually a very informative exercise. It engages the executive team in decision making to decide the non-negotiables, and then provides those decisions as established parameters for future transactions. It will also highlight key dependencies that may have been previously hidden. For example, if email integration is imperative due to the use of email for emergency notifications, investigate whether network integration is required as a facilitator for email integration. It is not uncommon for these critical path items to manifest and create a quite extensive minimum TOM. Insights into how extensive the minimum integration requirements will inform your decision process, both in regards to what kinds of deals you should pursue, and also what internal initiatives should be explored if acquisition is to remain a key component of your growth strategy. Recall that we discussed in previous chapters how back office structure impacts TOMs? If you plan to grow by acquisition and use extensive outsourcing and/or automation in your back office, you will have a more involved minimum TOM due to the high number of dependencies in such a model. In this case you could consider deciding to restructure the back office to add in additional flexibility to accommodate acquisitions. Alternatively, you could adjust your valuation models to accommodate higher costs to achieve, recognizing that doing so may reduce the number of deals in which you will be a competitive bidder. Either way, the minimum TOM exercise brings these choices out in the open, where they can be considered and addressed. If your company needs to do innovative or extra-accretive transactions routinely, then it will be critical to have a defined minimum TOM, and to ensure that your back office has the flexibility to accommodate these transactions. Full Integration TOM In a full integration TOM the acquired company disappears, and the acquirer’s model has the same 5w’s as it had prior to the transaction. Simply put, it describes the model whereby the acquirer completely absorbs the acquired into their standard organization design, tools, processes, and facilities. There are two critical points to remember when it comes to full integration TOMs. First, if you have extensively used outsourcing and automation there may be little difference in your minimum and full integration TOMs. This may indicate that you can realize value only from deals that will be fully integrated. It follows, then, that deals that rely on extra-accretive revenue synergies would not be a good fit. Companies in this position are largely limited to overlapping and some types of complimentary deals and must use other strategic transactions to achieve innovative growth. Second, the cost of integrating an acquired company into your existing target operating model will bear no resemblance to the current run-rate costs. This may sound obvious, but I continue to see deal models that assume existing run-rate costs, or run-rate plus an escalation factor, perhaps computed as a percentage of accretive revenue. Either approach completely ignores the costs of actually executing the integration program. We will go into the calculation of costs to achieve in more detail in later posts. It takes a substantial effort to prepare a full integration TOM that includes all of the components discussed at the beginning of this post; however, for the serial acquirer the investment is worthwhile. A properly designed full integration TOM can dramatically reduce the time it takes to fully integrate, aid in calculating costs to achieve for valuation purposes, reduce integration program costs, and provide program-wide visibility into the critical path and dependencies. Furthermore, this model is easily converted into a standard workplan and baseline program budget, both of which can then be “rolled up” with similar documents for other acquisitions, providing enhanced management visibility. Partial Integration TOMs If your back office has a flexible structure, and you plan to do a variety of deals, it can also be useful to define some standard partial integration TOMs. For example, at one prior client we employed 2 partial integration TOMs in addition to our full and minimum TOMs (for fun we referred to these as the Party Sub, the Footlong, the 6-Inch, and the No-Soup-For-You). The difference between the 2 partial TOMs largely hinged on whether the acquired company would be integrated into the parent company’s IT network, since network integration was required to access many of the standard tools and programs such as email, benefits, and procurement. With the 4 models defined, and estimating tools in place for each, we could very rapidly estimate the effort-hours, timeline, and costs for deals using a standard tool, and incorporate this information into the deal evaluation. Also, by using the same tools each time, we were able to identify areas where the models needed adjustment and thus improve them over time. Recap Standard TOMs are a useful tool for any company that plans on routinely using acquisitions as part of its growth strategy. Preparation of standard TOMs will discover critical path dependencies, as well as inform management about the ability of the current back office structure to accommodate each deal type. Last month we introduced the concept of selecting a target operating model, or TOM, based on the parameters of the deal. In this month’s post we’ll take a deeper dive into how this would apply to a vertical transaction, such as AT&T’s proposed purchase of Time Warner, Inc. Recall that we previously stipulated most acquirers will lack the knowledge, tools, and relationships to effectively manage a vertical acquisition. As such, most vertical deals will require lower levels of integration until enough internal expertise can be developed to make effective choices about how (or whether) to combine the companies. This means the acquirer is likely to have both an interim and an end-state TOM. The interim TOM describes a stable point in the integration where the companies will “pause” integration, operating in that TOM state until such time as additional integration becomes appropriate. Of course, if the businesses are different enough, it may never be practical or appropriate to integrate fully, in which case the end-state TOM becomes minimal integration, and an interim model is not required; however, in this case the overall return on the deal is at risk. The valuations of most vertical deals rely on either extensive cost or extra-accretive revenue synergies to justify the purchase price, and these synergies can be very difficult to achieve when companies continue to operate as separate entities. In the case of AT&T’s proposed purchase of Time Warner, Inc. it seems unlikely that AT&T’s internal organization design, systems configuration, and capital allocation cycle are ideal for media content production. AT&T has no content production expertise. Nor do they have any of the valuable relationships on which media producers rely. Some integration will be required to meet the minimum compliance requirements, such as being able to file SEC reports. And there may be some low-hanging fruit, i.e. standardizing on a common payroll provider and/or employee benefits platform, laying off some administrative employees, squeezing a few common suppliers for lower costs, but largely I would anticipate the companies continuing to operating independently should the deal come to fruition. What then will that mean in regards to AT&T realizing the synergies from the acquisition? Let’s first consider a simplified example with two imaginary companies. Cones, Inc. manufactures cones which it sells to its only customer Cream, Inc. an ice cream manufacturer and retailer. Prior to combining their business results are as follows:

Cream, Inc. decides to buy Cones, Inc. to reduce input cost for cones in their ice cream parlors. Comparable companies are selling for 10x revenue, so the purchase price of Cones, Inc. would be (200 x 10=2000). Since Cream, Inc. lacks the knowledge and equipment to make cones, they decide to let Cones, Inc. stand alone. After the acquisition operating results would be:

Cream, Inc. gets a boost in operating profit from $300 prior to the acquisition to $350 ($500-$150) after the acquisition. The combined results do not change since the operations are the same as before the combination; furthermore, Cream, Inc. must recover their cost of acquiring. If they wish to recover that cost over 5 years, they would need ($2000/5=$400) in benefits per year. This of course assumes that attorney fees, bankers, auditors, and other transaction costs were zero, and also ignores the time value of money. Even if Cones, Inc. had additional profitable customers, we would still have only accretive synergies if we persisted with maintaining separate operations, and the valuation would have been proportionately higher.

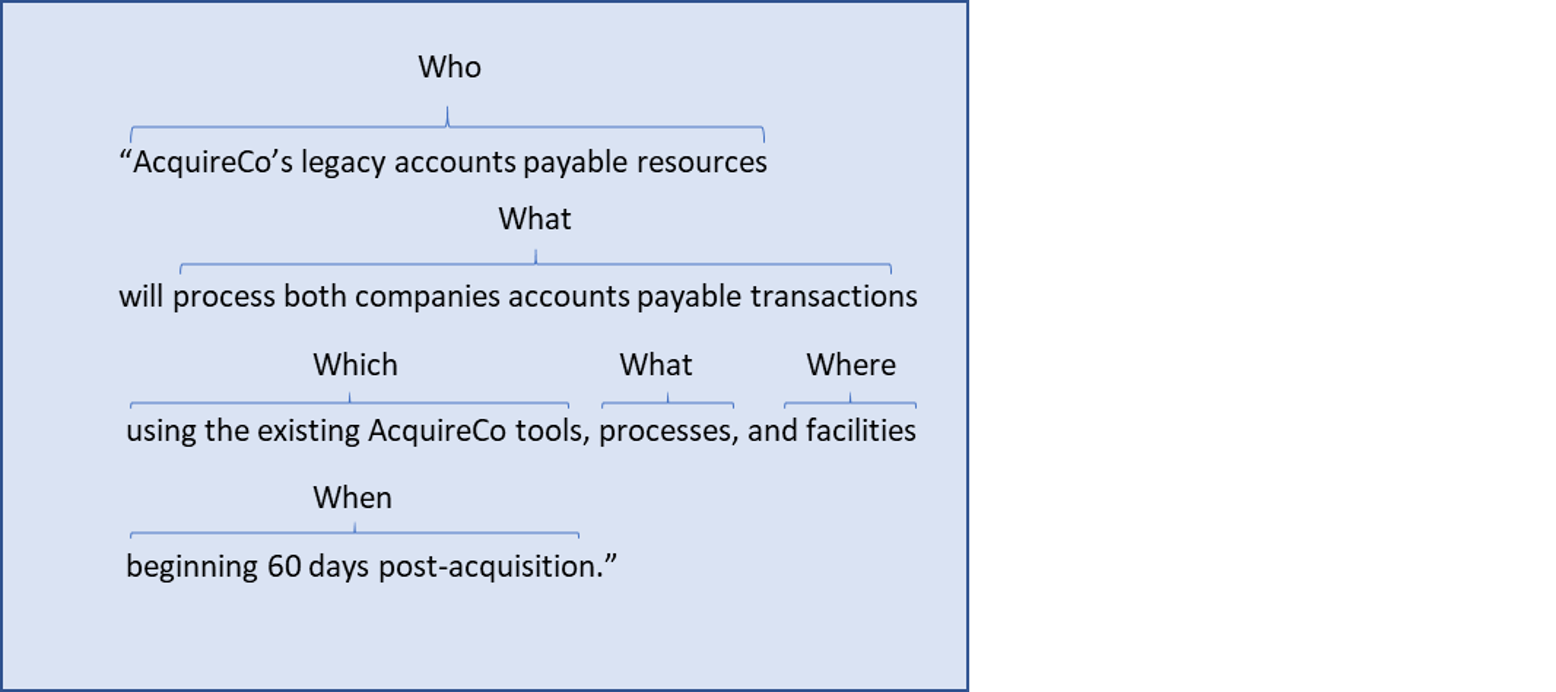

Now consider this example in light of AT&T’s proposed valuation for Time Warner, Inc. of 3.7 times revenue, and 27.8 times earnings, and it should become apparent that my bias against vertical deals is not merely the result of irrational prejudice. The bottom line is that unless a profitable business is being very inefficient in its operations or has a high cost of capital it is very difficult to realize extra-accretive synergies at all. Such synergies come from combining either cost structures or market offers, and often this is just not practical. Vertical deals will still take place, and AT&T’s consideration of Time Warner as a defensive move against Comcast’s acquisition of Universal is an example, but for most business vertical deals should be approached with a high degree of skepticism. The difficulty of combining non-overlapping businesses will likely delay synergy realization, and the purchase price, combined with costs to achieve extra-accretive synergies, make these very tricky indeed. Introduction Last month’s post wrapped up our “Deciding to Acquire” category for 2018. This month we’ll begin a new series of posts entitled “Selecting Target Operating Models” where we’ll explore how to choose our approach to integration based on deal parameters. Definition: Target Operating Model A Target Operating Model, or “TOM” describes the interim or end-state of both the acquirer and the target post acquisition. A well-crafted TOM describes the “5 W’s” as laid out in the following question: Who will do What, from Where using Which tools, and When? In this structure the “who” describes the personnel pool. Will it be legacy target staff, legacy acquirer staff? Both? Neither (i.e. we are eliminating the positions and outsourcing)? The “what” describes the business processes to be executed, including any net new processes, and/or adaptations of legacy processes. “Where” indicates the facilities where the resources (the “who”) will work, while executing each process (the “what”). Again, facilities may be legacy acquirer, legacy target, or net new. “Which” indicates the tangible and intangible assets used in the post-deal environment. Are we consolidating on a common enterprise management system? Are we going to continue operating on legacy contracts, or will we attempt to novate or otherwise establish common contractual agreements? Finally, “when” indicates the time period where the target operating model begins and ends. Many deals will integrate directly into their end-state operating model; however, there can also be cases where both an end-state and an interim model are appropriate. In this case, the “when” will describe when the interim model ends, and the end state model begins. Putting all this together, we get assumptions for each workstream that sound something like this:  Such TOM sentences become important assumptions about the deal. For example, it would be reasonable to assume from the example above that we can anticipate synergies from the elimination of the target’s accounts payable team, the facilities they work in, and the tools they use, but we will also have:

Deal Rationale Considerations and TOM Selection Recall from February’s post that we identified 2 basic categories of deals:

As we stipulated previously, these categories are highly generalized for purposes of this discussion. Additionally, it is common for acquirers to anticipate both cost and revenue synergies for a given transaction; however, one of these will, in fact, be what we call the primary value driver, meaning that this synergy addresses the strategic deal rationale. Overlapping deals will usually optimize at full, or nearly full, integration. This is because a greater degree of integration scope generally maximizes cost synergies by providing for the elimination of duplicate “W’s” (who, what, where, which) per our “5 W’s” model. Additionally, revenue synergies tend to be either unaffected or even optimized at higher levels of integration. For example, additional revenue synergies could result from cross-selling, raising prices, bundling offers, etc. The greater the overlap between target and acquirer, the more this tends to hold true. Complimentary deals have much greater variability in optimal TOMs, but there is a general rule that can be applied: The greater the level of innovation or creativity implicit in the revenue synergies, the lower the level of optimal integration The table below provides a general outline of where most complementary deals will optimize:

Many companies underestimate the challenges with learning to operate in new geographies, and university case studies are full of such examples. If geographic expansion is the primary driver of deal rationale, the best approach is usually to do a minimum amount of integration initially, and to stabilize on an interim TOM. This allows the acquirer’s management to focus on gaining share in the new market and achieving the revenue synergies, without the distraction of adapting back office systems and processes to adequately address any new compliance or operating requirements. Furthermore, retaining the acquired in-country staff allows the acquirer to benefit from their local knowledge and networks.

Portfolio expansion deals usually benefit from moving straight to full integration, provided that the products being added have reached a level of maturity where innovation is not a primary concern. Integrating fully facilitates joint management of product and offer portfolios, and thus helps with revenue synergy realization. And of course, as with all full integration TOMs, and available cost synergies will also be realized. Innovative deals are a real challenge for most companies, particularly public companies with heavy compliance requirements. The temptation to integrate- and thus realize cost synergies while simplifying back office processes- will be difficult to resist. Just know that the track record of companies that integrate their innovative acquisitions is poor indeed. Key talent gets recruited away, disruption in tools, processes, benefits, or facilities creates a distraction that hampers the innovative process. Upon integration the combined company often looks a great deal like it did prior to the deal, with no noticeable increase in innovative capabilities. Correspondingly, the same pitfalls apply to acquisition of immature product offers that still require “care and feeding” from their development teams. Bottom line: if you are lucky enough to buy a goose that lays golden eggs, resist the temptation to remodel her nest! Conclusion Choosing the right TOM is a vital component to crafting a realistic approach to due diligence, valuation, and synergy realization. Over our next few posts we’ll continue to expand on selecting and formulating TOMs for different deal types, and we’ll explore how various corporate structure and operational considerations impact our choice. We look forward to hearing your thoughts, K |

Archives

July 2020

Categories

All

Sign up to receive a free 30 minute consultation and our "PMO in a Box" toolkit!

|